Summary Block

- for speed listening, go to the settings wheel on the bottom right of the video and choose playback speed - after one minute video becomes high-resolution -

Capital Structure - 2 Sep 25

Fundamentals - 2 Sep 25

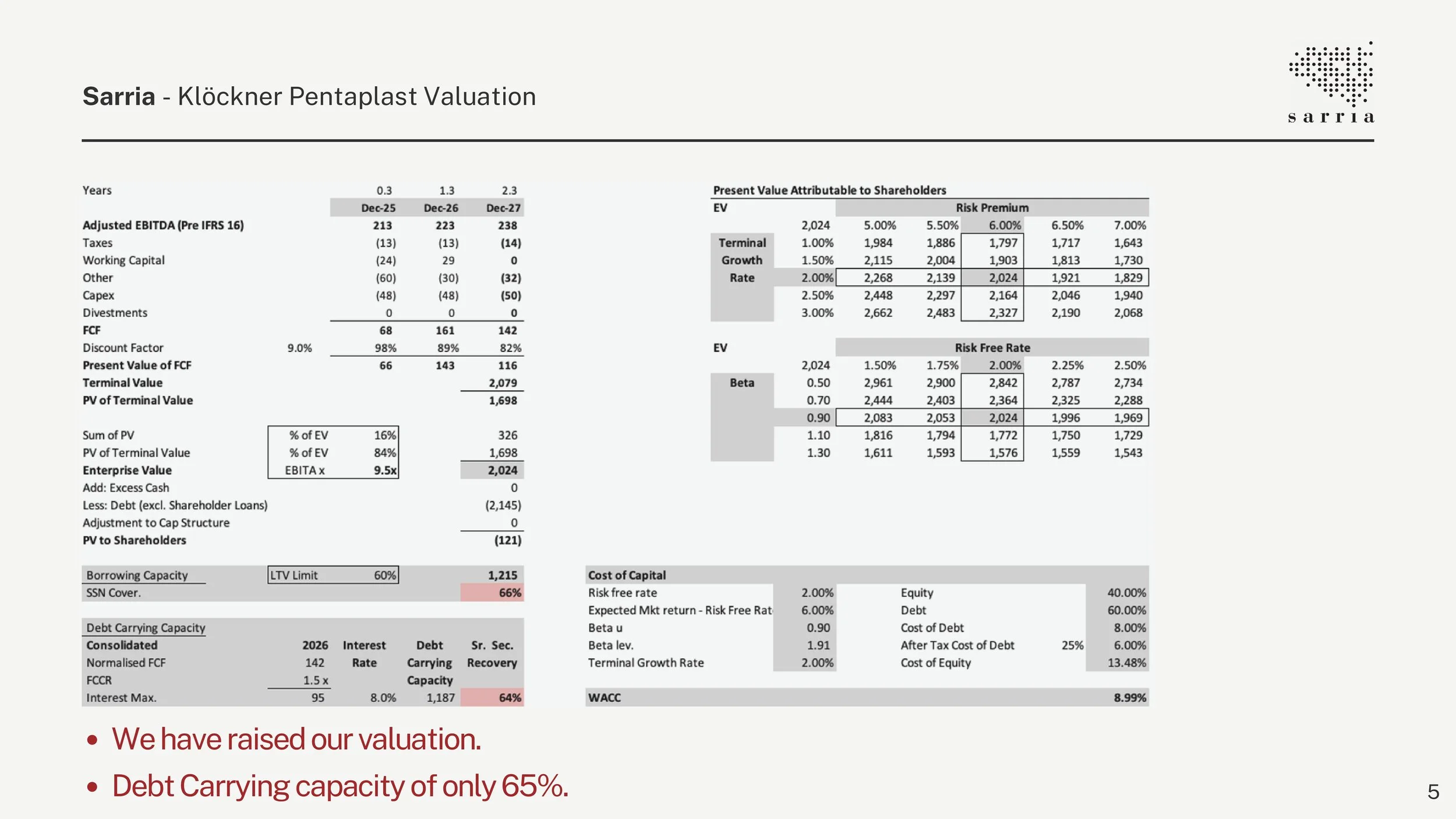

Valuation - 2 Sep 25

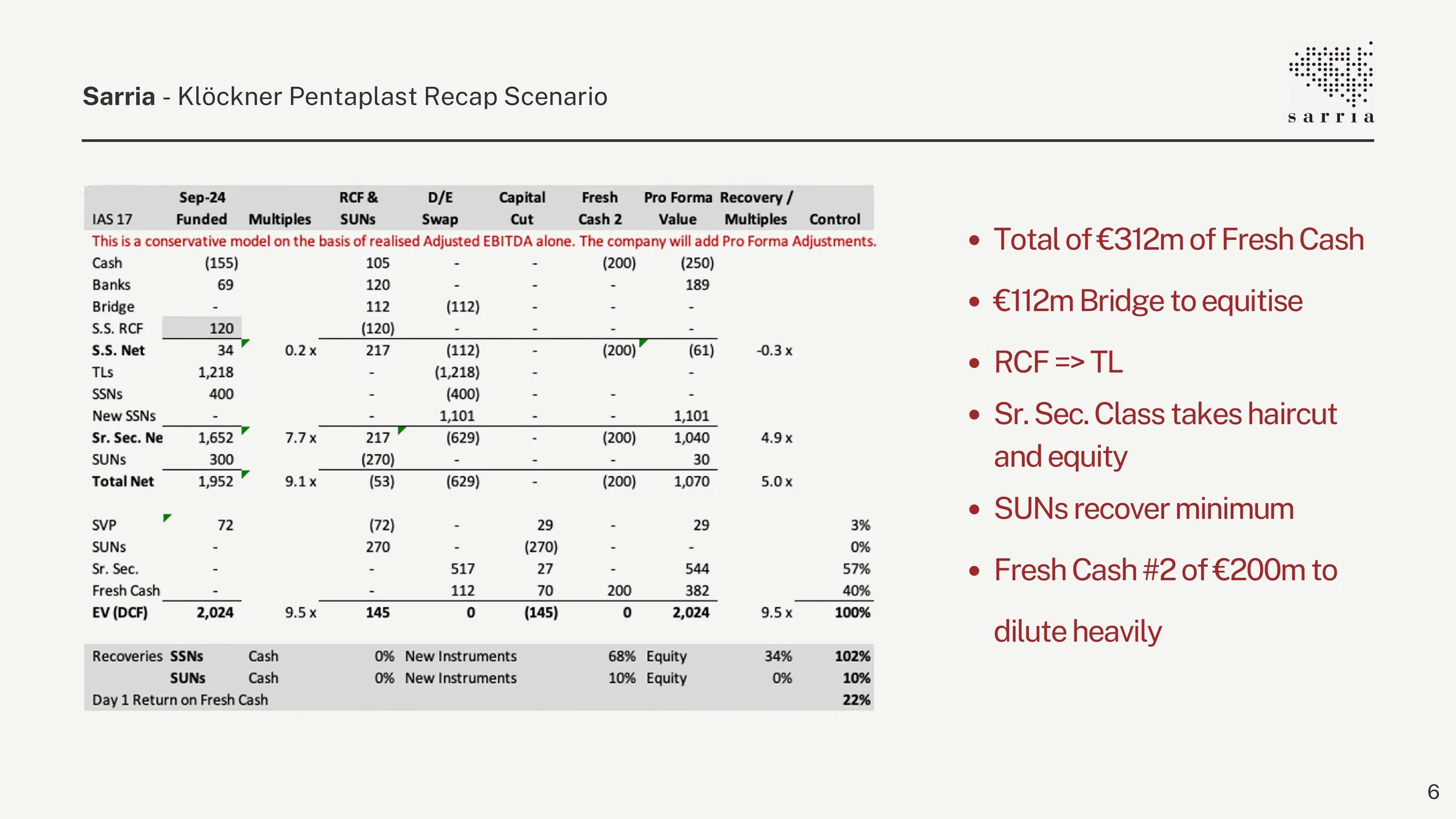

Recap Scenario - 02 Sep 25

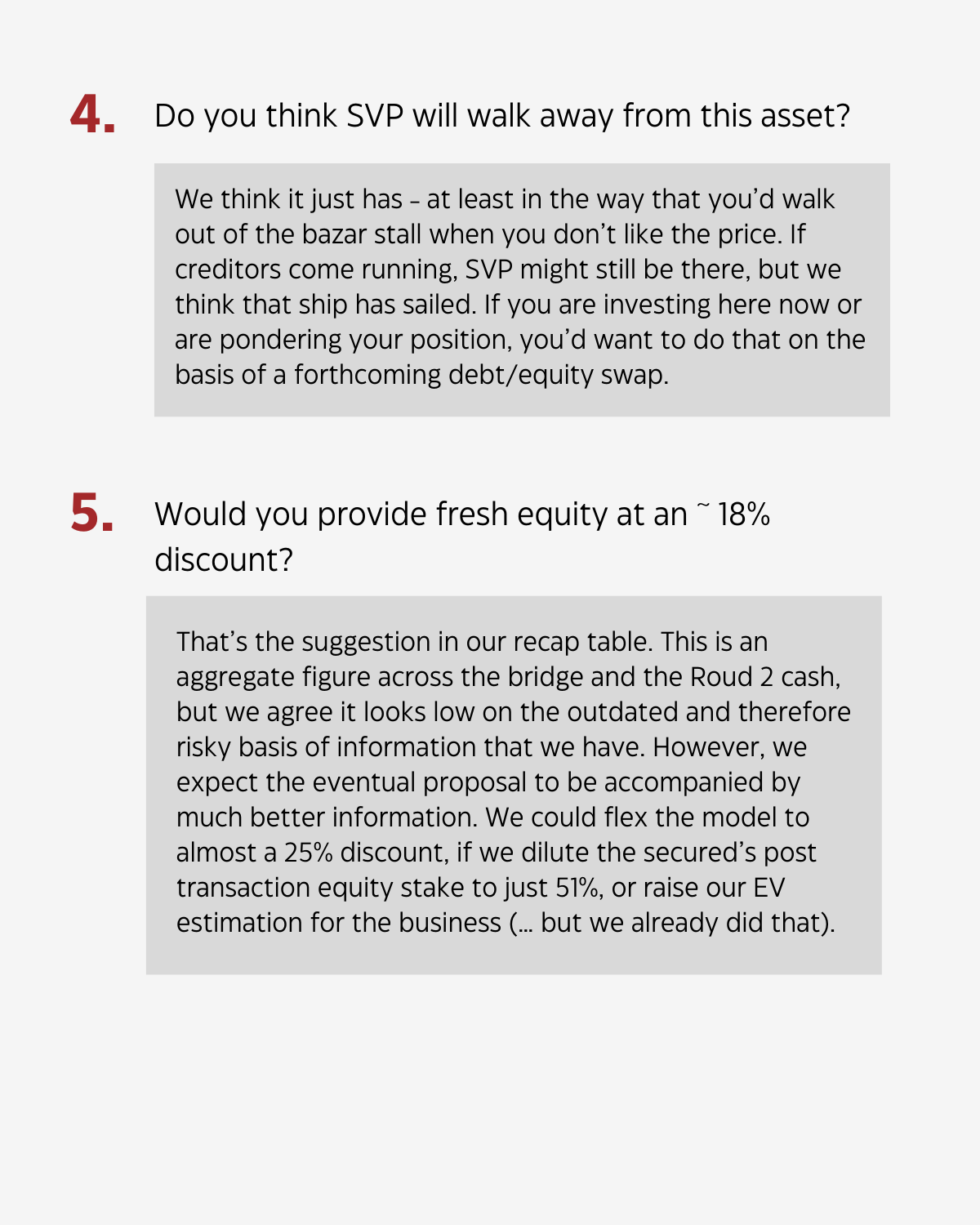

Investment Discussion - 2 Sep 25

Presentation

Q&A

Initiation

Intro, Legal and Cap Structure - 28 Jan 25

Investment Discussion - 28 Jan25

Company and Industry - 28 Jan 25

LONG Idea

Model and Drivers - 28 Jan 25

Valuation and Recap Scenario-28 Jan 25

SARRIA News -INTU