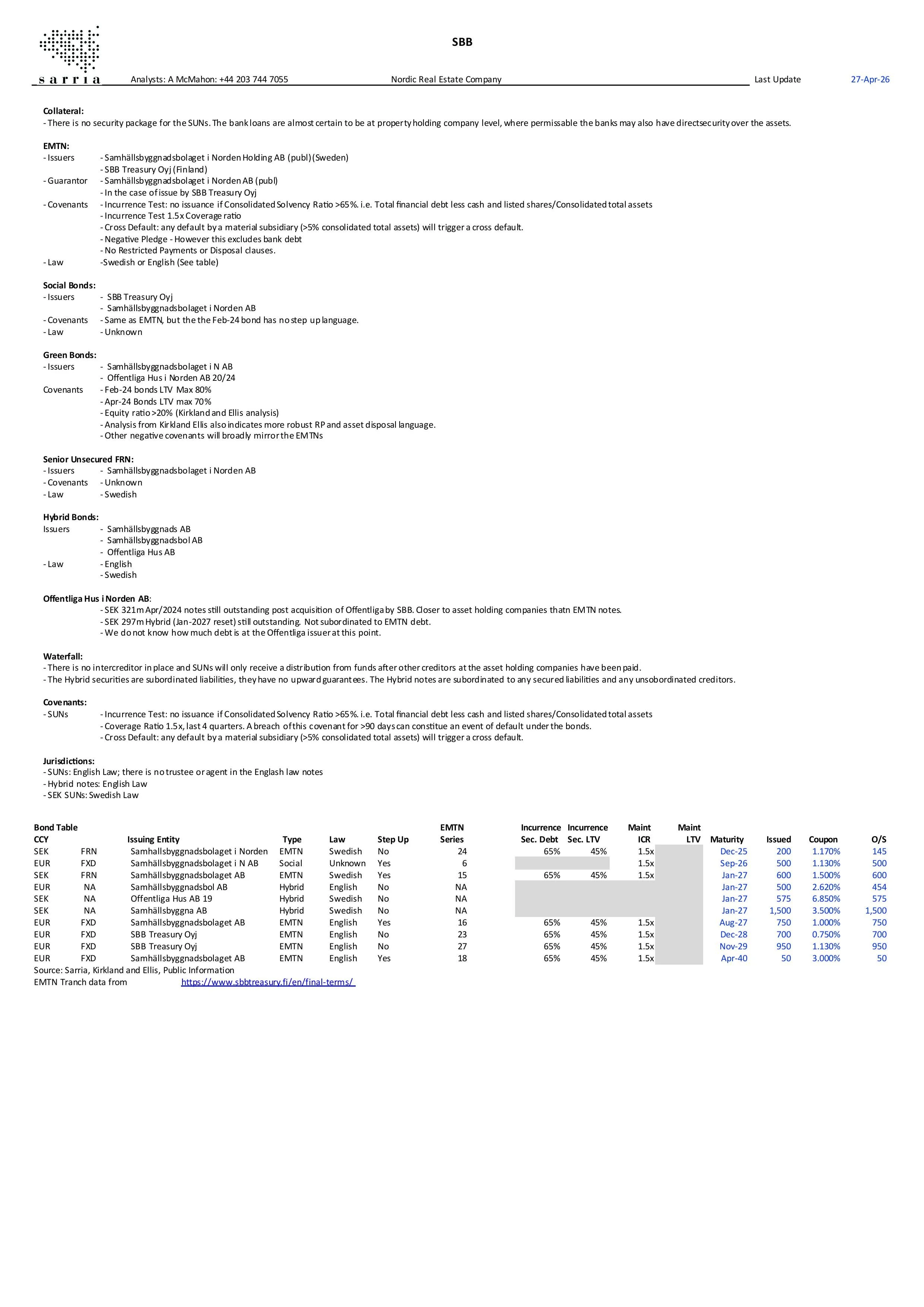

Summary Block

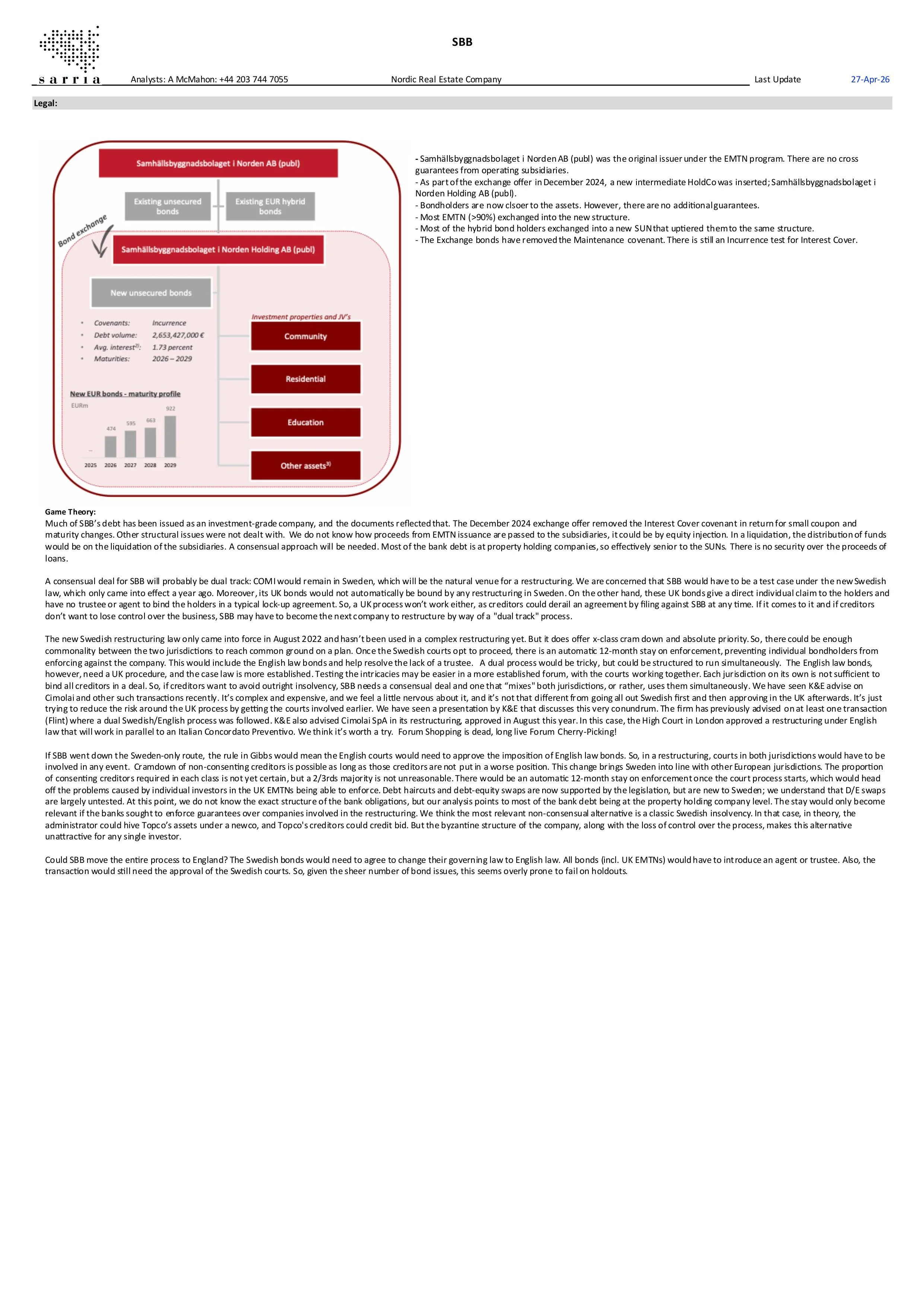

Intro, Legal and Cap Struct - 31Mar23

Real Estate Business - 31 Mar23

Ed.Business and Invest-31Mar23

Value Buckets - 31 Mar 23

Maturities and Layering-31Mar23

Investment discussion-31Mar23

Featured