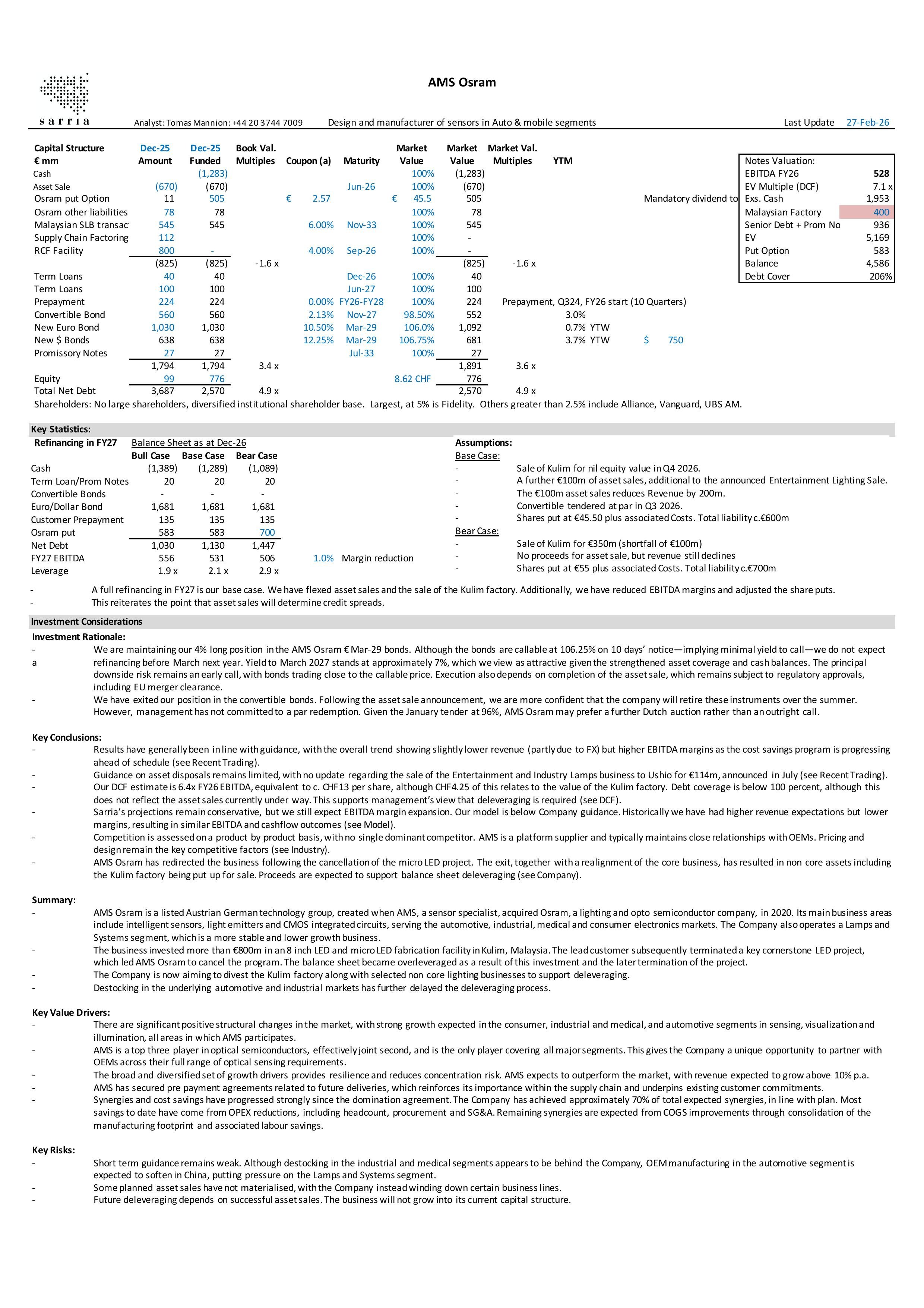

Summary Block

LONG Idea

- for speed listening, go to the settings wheel on the bottom right of the video and choose playback speed -

Update Positioning - 8 May 2024

Intro, Capital and Legal Structure 26/01/23

Company and Merger 26/01/23

Cash Flow and Model 26/01/23

Investment Discussion 26/01/23

Featured