Client Calls | Events

Best Ideas

Intrum LONG Idea

Flora LONG

AMS LONG Idea

Maxeda SHORT Idea

ION Platform Long

Rekeep LONG Idea

Transcom Long

Flora LONG Idea

Antolin Long/Short

Vivion LONG Idea

Mobico LONG

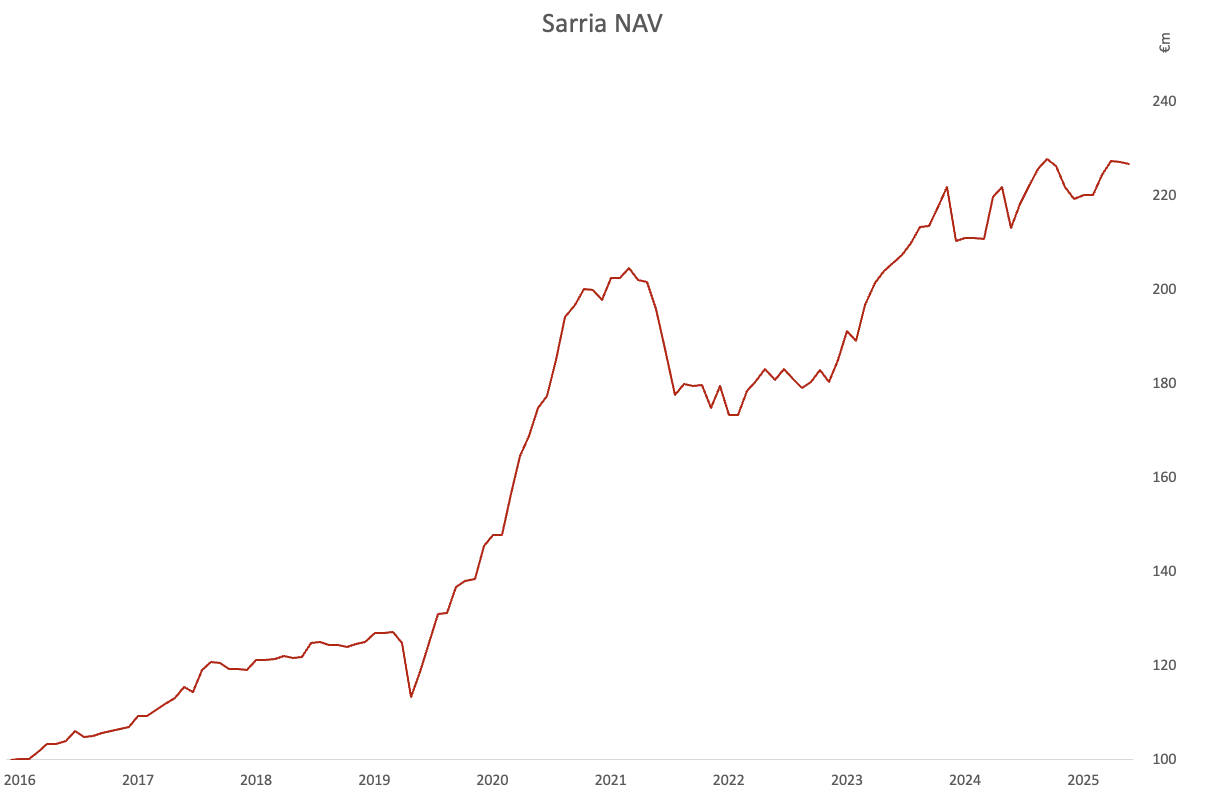

Sarria Nav - April 2026

YIELD based risk profiles

-

Adler: The 1Ls and 1.5Ls are value covered at 60% and 80% through the structure. The 2Ls are the fulcrum. The structure will have to be renegotiated in 2028 unless management can find an exit for all its assets by then.

The 2Ls yield 9% if Bunds remain at their current levels. If 2-year Bunds, for instance, tighten from the present 2.15% back to 1.8% (some mean reversion), then yield should reach 20%.

-

ams OSRAM: AMS Osram’s credit profile has fundamentally shifted following the pending asset sales. The capital structure now clearly points toward refinancing, and pricing of the outstanding bonds largely reflects market assumptions around the timing of that refinancing.

Convertible bonds @ 97.5c/€, the convertibles offer limited upside of 2.5 points with minimal carry given the low coupon. Upside improves if the company calls the bonds over the summer, which remains our base case, and we see no realistic scenario in which the convertibles remain outstanding beyond March 2027. The downside stems from the risk of a further Dutch auction and a refinancing alongside the high-yield bonds in March next year.

High-yield bonds: Our base case assumes refinancing in March 2027, when call protection steps down, implying a yield of c. 7%. The principal downside risk lies in an early call, as the bonds are currently callable on 10 days’ notice at par plus coupon, which would leave investors with minimal return.

The successful completion of the asset sale to Infineon remains critical. We see no reason for the transaction to fail; however, any delay or cancellation would undermine the core deleveraging strategy and likely push the bonds below par, resulting in distressed pricing.

-

Ardagh: The 1st and 2nd Liens are trading at 97%, and we see up to 6 points of upside in the 1st Liens over the next 12 months. The 2nd Liens should trade 150bp wide of the 1st Liens, so we see 3 points of downside and 3 of upside in the same period. Our valuation on the equity would give SUNs holder a recovery of only 23% today, as we expect it will take three years for Ardagh to be in a position to be sold on the public equity market. Operationally, Ardagh will take time to recover from what has been a difficult three years. We may revise our model upwards towards the end of 2026, if the company is outpacing our expected recovery, but not yet.

-

ASDA: We see the best potential value in the EUR700m 2031 SSNs, currently trading at 93.75%. We see little short-term upside and 2/3 points of downside, but over the next 9 months, there are 7 points of upside (YTW 7.75%), and 5 points of downside (10.5% YTW) as ASDA starts to deliver some traction on bottoming out its sales. The GBP SSNs trade at 92% (10.6% YTW) and have similar upside/downside characteristics. Concerns about inflation in the UK will drag on the SSNs in the short term. Once some progress is shown in the Q1 results, we expect the bonds to rise.

-

Aston Martin: At 89p/£ the SSNs are beginning to look attractive, but there is too much risk of further disappointment on the Q3 call (29th October). We expect a GBP200m cash raise to be announced at the time of the call to bolster cash reserves and see 5 points of upside. However, if the cash delay was delayed, we could see up to 5 points of downside. The company also needs to provide more clarity on its outlook for unit sales and profitability in 2026.

-

Atos:

1L: Under most scenarios, the 1L is fully covered. However, trading at 111%, with a YTM of 11% it offers limited upside. We expect 4pts of upside if better numbers materialise, leaving yields at 10% to maturity. However, any early take-out reduces the yield, with take-out in Dec-27 on the back of strong numbers, the yield falls to 7.6%. The downside is limited for the 1L, but with slightly weaker guidance for Q3 revenue, we expect a more favourable entry point.

1.5L: This is the real fulcrum instrument, with variations in operating margin and restructuring costs resulting in either 2x covered or zero recovery. The current 14% YTM at current prices is not sufficient for that volatility, and we view a fair price 20pts lower at 63% (20% YTM). Upside is potentially 10pts to an 11.5% YTM, but that would require some substantial margin improvement and a significant reduction in cash restructuring costs.

2L: A pure equity instrument, which at 4.3x LTM leverage, is barely in the money. The buy-in multiple is c.4.0x. This instrument will not see any major upside in the short term due to the substantial restructuring still required.

-

BioGroup: Upside: Limited in the near term due to uncertainty around France’s future pricing regime. On favourable clarification from the French state, bonds could rally to a c.6% yield (5pts upside), but we do not expect clarity before late Q3, capping near-term gains.

Downside: Highly sensitive to the pricing outcome. In an adverse repricing scenario, yields could widen to c10% (c.10pts downside).

-

Birkenstock: The bonds are trading at the 2026 call price (April 2026), and the upside is limited. We see three points of downside if the global economy goes into reverse. The equity cushion of $3.1bn makes distress highly unlikely. The company may call the bonds in April, but for a saving of 100bp in coupon, Birkenstock is more likely to repay another piece of it, €/$ TLB.

-

Boparan: We see little upside, as the bonds are callable at 104.7 from July 2026, and currently trade around 105p/£. We see potential for 6 points of downside (YTW 10%) if Poultry customers begin to pressure Boparan on margins, but do not see this as an imminent risk. Boparan has a long history of leaning on its customers/suppliers as it approaches a refinance and giving ground back after the new bonds are issued, and we see history repeating itself, but it will take time. Q1 results are out on 22/12/25, but we do not expect there will be much new news at that time.

-

Clariane: Unsecured: At 7% yield, we see limited downside in the medium term. The structure has broadly tightened over the last 6 months, with the Company tapping its recent June issuance to improve liquidity. Further tightening is possible with occupancy rates continuing to improve. At 6% yield, the newly issued bonds have 4pts of upside.

With this background, the Hybrid bonds offer a 13% yield which remains attractive, despite it subordination. There remains a significant equity cushion beneath, and with improving operational stats, the hybrid bonds provide decent risk-reward.

Downside centres on the current uncertainty with the French government and the broader impact on French yields. The Unsecured could trade down 4pts for an 8% yield, but the high coupon on the Hybrids are likely to limit any meaningful downside.

-

CPI Property Group: Risk Summary (BB+ Negative outlook) Green, Yield Name CPI’s SUNs are trading between 5% and 5.5%, and the portfolio is yielding over 6%. CPI has already accessed the Capital Markets at yields of 5.5% - 6.0%. CPI is not going to feel pressured into refinancing, as the latest deals saw debt yielding 5.5% replacing debt yielding 1.625%. We see maybe a point of upside, and two of downside in the 2030 SUNs. The pick-up yield to the newly issued Hybrids is inside 200bp, but these may well be tightly held, so a short is unlikely to cover the bid offer spread.

We do not see an imminent return to IG ratings at CPI, but the 3.75% July 2028 Reset bonds will be targeted once the rating increase is achieved. The 2028 hybrids trade at c90/€, we don’t see the trade as compelling, but we will review it in Q1 2026.

-

Consolidated Energy - At 92.3c/$, we see the most value in the 12% 2031 SUNS as they will benefit from both spread compression and improved operational performance. We see 12 points of upside (with the bonds trading at 11%) in the next 12 months. If the global economy weakens, there are six points of downside. The Proman loan has been repaid via a mixture of Cash and assets, and the new TLB has provided the cash needed to refinance the May 2026 SUNs. The CEL SUNs were layered by this new TL B, but this was priced into the bonds already. Whilst Methanex will eventually want to control the Natgasoline plant, we do not see any imminent change in either ownership or operational control

-

Engineering Group: Upside in the SSNs is limited to 2 points due to callability, and whilst we see 6 points of potential downside, we do not see a near-term catalyst for the downside to occur. If non-recurring costs continue, we would see the 2030 SSNs as a potential short. However, our DCF calculation shows €700m of value beneath the bonds. Leverage is high (>5.5x) due to persistent one-offs, but management has said these should be ending. Having recently completed a refinance operation, Engineering has little by way of maturities, and cash on hand plus the RCF show good liquidity. Working capital swings are significant, and the reduction or withdrawal of factoring lines would cause a liquidity crunch, but we do not see withdrawal as likely. The company has a dominant position in the sector in Italy and should benefit from increased digital spending. Other Italian-based IT providers trade at multiples of 9x+ on the expectation that growth is coming.

-

Eutelsat: As €1.3bn of fresh equity come into Communications S.A., the bonds are trading tight. Management has already signalled it will address the front end of the curve, and from April, the expensive ‘29s become callable too and are trading call constraint.

Numbed to the pains at the GEO business, the bonds offer little upside or downside in the near term. We will reassess after the refinancings, as by 2028, we expect the business to require more cash again.

-

Fedrigoni: In the high single digits, the bonds offer little upside from their 96c/€ trading levels, compared with the likely scenario that Fedrigoni will exceed its maintenance leverage covenant while its other credit metrics are also softening. Considering its downstream links to the struggling luxury sector, low double digit YTMs would seem more appropriate, which would land the bonds 5 points lower at around 90c/€.

-

We expect the Senior Secured Notes to tighten modestly as incremental deleveraging progresses, towards a yield of around 7%, implying approximately 2–3 points of price upside. Including carry, this would translate into an estimated total return of 8–9% over the next 6–12 months. The subordinated bonds offer greater convexity, with potential to reprice towards a c.10% yield, equating to around 6–7 points of upside. In our view, the current yield differential between the two instruments appears wide relative to the incremental c.0.6x of leverage and could compress to around 400–450bps from current levels.

Downside risk for the Senior Secured Notes remains limited, in our view, at approximately 3–4 points, reflecting the absence of near-term refinancing pressure. Likewise, we see constrained downside for the Senior Notes, with the next maturity not until July 2029. While the bonds were weakly placed at issuance, at current prices they offer an attractive c.15% yield for a credit with no imminent maturities and a reasonable equity cushion.

-

Grand City Properties: The unsecured trade tight, with limited upside. The Hybrids could trade a couple of points tighter, on a relative basis versus peers. However, this is unlikely unless the equity tightens the discount versus book value it trades at. The equity remains at a 30% discount to Book Value versus c.20% for other listed peers.

The downside for GCP from a downward asset revaluation is low. LTV for the Hybrids is 46% on Book Value. Assuming the equity markets value the assets perfectly, the LTV is 68% through the Hybrids, providing significant asset coverage.

-

Grifols: As a risk arb trade, under a change of control scenario, there are c.10pts of upside in the sub notes, with c. 8-10pts of downside. The only senior Secured Notes trading at a substantial discount to par are the 2027 Notes, which have 8pts of upside, with c.4pts of downside to trade in line with the other pari-passu notes that trade above par.

In the absence of a bid, the bonds trade at fair value, with seniors at 6.5% and subs 100bps back for an additional 1.5x of leverage. If the bid rumour dissipates, both bonds will trade down. We see long-term value at current levels.

-

Heimstaden AB

The bonds also trade very tight, and the structure offers limited upside at current levels. There is, however, scope for material downside should dividend flows from Bostad remain suspended for longer than expected. Offsetting this risk, continued progress with the privatisation programme is improving leverage metrics, and we would expect a rating upgrade during 2026.

-

Heimstaden Bostad : Both the unsecured bonds and hybrids are trading relatively tight. At c.4% for the unsecured and close to par for the hybrids, we see very limited upside from current levels. While there remains a potential downside risk should Alecta attempt a clumsy exit from its investment, we consider such a scenario highly unlikely.

-

HoHR: While HoHR has no fixed assets, its SSNs are deeply value covered and the FCCR should remain at or above 1x as the company turns around this year.

The wide coupon mitigates the downside despite the comparatively long 2029 duration, so that a 15% yield, for instance, is less than 10 points away from today’s price of 92c/€.

On the upside, we expect the bonds to return to near par within the year on news of the turnaround, which, together with the 9% coupon, should provide us with an IRR of 20%.

-

HSE At 99c/€, we see the SSNs as trading at fair value. We see little upside; holders will benefit from partial repayments at par from the cash sweep mechanism. The SSNs yield 8%, which is not bad, but with little upside and a refinance unlikely, we think there are easier ways to earn this type of return. The PIKs (stapled to an equity participation instrument) are trading at 51c/€; we see 16 points of upside and 10 points of downside in the next 12 months. FV is 77c/€, but this will take time, and the need to deal with the debt levels by 2029 will hold the PIKs back. With only €192m outstanding, liquidity will be tight and building a position challenging. We apply a distressed discount to our valuation; excluding this, there is some upside to our valuation, but we do not see this disappearing over the next 2 years.

-

Iceland: The call structure constrains upside, and while we do not expect a refinancing until the autumn, the bonds still offer some carry. On the FRNs, carry is 7.5%. However, the bonds are callable at 10 days' notice at par, 1pt below current trading levels. The 2028s are trading below par, so offer some protection. With the coupon at 4.375%, the yield is 5% YTM, rising to 8% if called this August. Downside appears limited, with a refinancing this year looking more a question of timing than feasibility.

-

Intrum: The bonds are callable at par in July 2027, so upside is beginning to be call constrained to 101c/€ if we assume a 7.5% yield, which still seems a while off. A 91c/€ downside of 12.5% YTM looks equally far away. This is no longer a binary credit and the ca. 10% yield look safe enough to us on what is now strong credit documentation (albeit on a service business where the Exchange Notes are no longer backed by owned ERC).

-

ION Platform: The bonds are currently trading at yields of approximately 10–11%, depending on maturity. We see the risk/reward skewed to the upside, particularly given the significant short interest heading into the Q1 results. With the Company demonstrating a willingness to repurchase bonds and improvements in investor relations, the risk of severe downside has diminished. From current levels, we see limited downside of a few points, which would imply yields widening to around 12–13%. Meaningful repricing toward rating-consistent levels will likely require clear evidence of realised synergies. As such, near-term upside appears capped at approximately 5 points, corresponding to yield compression to the 9–10% range.

-

Modulaire: Modulaire Q2 numbers were weaker than we expected, and utilisation rates are still low. H2 25 will also be weak as the UK and French construction markets remain soft. We expect recovery to be weighted to H2 26, but with €270m liquidity (between cash and RCF), Modulaire should not enter distress.

The 450bp pickup in spread from the €SSN to the €SUN is attractive, and we would expect that to reduce, but not yet. There are approximately 3 points of downside and 2 points of upside in the SSNs heading into the Q3 results. The SUNs will be more volatile with 5 points of downside and 5 of upside in the same period.

-

Morrisons: The SUNs trade 78%, giving a YTW of 15.5%. We see 5 points of upside in the SUNs to give a YTW of 13% and 3 points of downside for a YTW of 17%. The SUNs trade 350bp wide of the SSNs, which we see as excessive. The SUNs will not be called early, as there is a trigger clause in the new SSNs. We do not forecast any cash needs at Morrisons, but the unencumbered estate offers a significant opportunity within the 8.75% coupon paid on the £ SSNs last summer. - From the DCF, LTV is now around 70%, and the equity cushion is still significant. - We still do not see an all-out price war erupting, but we do see the current level of price support persisting for another 12 to 18 months. The launch of further discounts by Morrisons demonstrates that the pressure on margins is continuing.

-

Ocado We liked the 0.75% £350m Jan-27 at 80.5p/£, and we still like it at 91.2p. We do not expect this low-coupon instrument to be called early, but there will be a pull to par next year. We see 10 points of upside and little downside unless there is a significant negative re-rating of the credit. We also like the 11% Aug-30 SUNs at 95p/£, we see 5 points of upside and 5 of downside, but an 11% coupon makes the Total Return attractive on a 12-month hold basis. We value the retail business at 30p/£; the Technology business covers the rest of the debt. We value the equity at 212p, not far from the equity markets’ 225p. With the slower CFC rollout, we see the company issuing up to £300m of equity to bolster liquidity in FYE27.

-

OHLA: The SSNs are trading at 93.5% with a YTW of 12.5%. The upside is around 6 points (10% YTW), and the downside is 5 points (15% YTW). With a yield of 12.5%, the bonds look like a decent yield play, but OHLA is volatile, and management is highly opaque. The weak European construction market held back OHLA bonds in 2025, and Modulaire is probably a more reliable macro play. The US has been strong and will underpin the business in 2026. The expected cash sale of the Canalejas asset was another potential upside, but this has morphed into the assets being split between the partners.

-

Pasubio: Upside: A refinancing following the mid-June non-deal roadshow could deliver c.2.5pts of upside from current levels.

Downside: Significant in the absence of a deal. Market focus would shift to the over-leveraged balance sheet and the underperforming auto segment, which remains the core revenue and EBITDA driver. While likely to be gradual, without refinancing, bonds could retrace to the low-90s initially, with yields ultimately drifting to c.15–18% (implying prices in the low-to-mid-80s).

-

PizzaExpress: Operations are stable and, within the confines of the macro backdrop, PizzaExpress is reasonably profitable. At 2/3 of EV, we find the bonds attractive and are surprised at the low rating. There are worse credits being rated BB. Following the restructuring, we think the bonds should remain in the low 90s for a while, tightening with any growth in performance, which should be dependent on consumer demand only. We do not see more than five points of downside, given the significant coupon and stable operations.

-

Punch: Punch bonds trade at 7.3% yield to last call in 2029 as the company is doing well after several tough inflation years in which other pub formats fared worse. Upside is limited to perhaps two points by the first call date in 2027. Downside could come from a large dilutive acquisition or a dividend to Fortress. Either is likely, and management have already indicated to be looking for targets. The large Platinum estate of Stonegate is for sale. Current minor pub acquisitions are non-dilutive at 6.5x, but a larger acquisition could be more expensive.

-

Rekeep: The bonds are unlikely to see any meaningful upside until there is clarity regarding the investigation in Palermo. A minor fine would likely prompt a recovery, although the bonds are unlikely to approach par without progress on an asset sale. Operational performance has shown some positive momentum, but with the investigation ongoing, there is no short term catalyst for upside.

Downside is also contingent on the investigation. Based on precedent from the FM4 case, we estimate that any fine, if imposed, could be approximately €1m to €2m. The more material risk would be a prohibition on tendering for new contracts, which could result in an additional 10pt decline. This risk is partially mitigated by the potential for asset sales.

-

SES / Intelsat: Margins are falling faster than revenues can stabilise; that seems to be more than just the effect of the Oi insolvency. As such, we see technically only five points of movement either side in the 2.875% Perps next month (Q126 results), but medium term, we are concerned that the interest coverage could deteriorate quickly (see the high operating leverage), despite the SPACE transaction that effectively swapped SUNs for Hybrids. We thereforefind the 5% downside far more likely than the 5% upside and could imagine further downside as low margin new business must replace the high margin business that’s leaving to Starlink.

-

The Very Group: At 98%, The Very Group bonds yield 8% to maturity (August ’26) but offer some additional upside from an early take-out. This is driven by debt held by Carlyle maturing in November 2025 at one of the myriad holding companies outside the restricted group. Asset coverage is sufficient to meet not just the bonds but also the Carlyle debt, which is solely secured on the equity of The Very Group.

The downside will be gradual, likely prompted by further deterioration in retail sales. There is the potential for an increase in default rates, but given the long history of strong repayment profiles of its customers, we see this as low risk.

-

Travelodge: The 10.25% 2028 GBP SSNs are callable at 102.563 now and at par from April 2027. The EUR FRN is callable at 100.5 now and Par from June this year. Trading at 96%, upside in the GBP SSNs is 7 points and downside is 4 points (trade out to 15%). The Sonia +3.75%2030 FRN trades at 92 and has 8 points of upside and 10 points of downside (trading out to c12%).

Travelodge will wait until they think they get a lower coupon before refinancing the £415m April-28 SUNs. Getting a better deal on the 2030 FRN margin is unlikely in the current environment, so it will be left in place for now.

-

Viridien (CGG): Viridien has refinanced its SSNs, pushing maturities out to 2030; the SSNs are already trading at or above their 2027 call prices. Upside is limited as the bonds are call limited. The downside is 5 points (YTW 7.5% on the €SSN) if oil prices fall beneath $50 a barrel, but this is not something we expect. The family rating of B and the bond rating of BB- will attract bids from CLOs. Management has said it intends to call 10% of the bonds in 2026 and 2027 at 103 in accordance with the bond indenture, which means the bonds are trading point lower than they would be absent the call feature.

-

Vivion: Vivion is still a macro play on continued recovery in RE valuations, bolstered by rate cuts. The 2029 bonds yield 9.5% (including 1.5% PIK). We see 8 points of upside if the company proceeds in getting new investors and/or falling rates push valuations higher. We see 6 points of downside if the current tariff rows stoke inflation. Vivion has pushed its bond maturities out to 2028, and privately placed €250m in additional 2028 bonds back in December. With €544m outstanding, we expect good liquidity in the 2029 bonds. The next catalyst will be the publication of H1 25 results in mid-September.

-

VMEDO2: The EV comfortably covers the debt stack, and 9% for secured paper is not a bad return vs bank deposits or IG Paper. Also, there are no significant maturities until 2028. We see three points of upside/downside (+/- 100 basis points in yield) in the 2030 SUNs. This will be driven by moves in the underlying interest rates rather than a fundamental change in VM02’s credit risk. These are low-coupon instruments, so VM02 is not going to redeem them early. In terms of operational risk, even if the war in the Gulf drags on, we see the main friction as being in Pay TV, which is a low-margin product for VM02.

-

Worldline: The short-term maturities are safe. But at 9% YTM the 2028s and beyond risk being forced into an A&E or worse. It is too early to speculate on any valuation floor, but without fixed assets and Worldline being in a strategically difficult position, there is no downside protection to the bonds.

The market has far better risk for these returns.

EVENT DRIVEN risk profiles

-

Accentro: The SUNs are trading at c40%, and we value the package being offered to SUN holders at 32%, so we see eight points of downside to the current price. Failure to execute the restructuring is unlikely. The transaction will convert 35% of the SUNs to SSNs, with the remaining 65% reinstated as deeply subordinated notes. There will be €77m of New Money, which will be Super Senior and will get 86% of the equity. Accentro will utilise the StaRug process to obtain court approval, and the Ad Hoc Committee already represents 80% of the outstanding SUNs (75% needed for court approval). The transaction is due to be completed by the end of September 2025.

The immediate upside is limited, but longer term, we see significant potential in the underlying assets, particularly the Inventory in Berlin. However, we will need to see the publication of audited numbers, which is likely to occur after this recapitalisation completes.

-

Adler Pelzer: The bonds are due in April 2027, trading at 90c/€ today.

For the 10 points of upside + 1/2 a considerable coupon investors risk either of the two downside scenarios: 1) the deal does not come together and bonds drop into the 70s on uncertainty, before perhaps eventually recovering to fair value in the 80s, or 2) the refi/A&E is successful and the bonds drop towards fair value on the other side of it - perhaps too soon to get out with the gain in hand.

-

Air Baltic: It’s too early to gauge the outcome of the forthcoming Air Baltic restructuring. Latvia could inject the cash and keep creditors whole. That would save its reputation and ensure its continued development towards the West, to which it is otherwise only connected by sea. Narrower already is the path along which Lufthansa pays for the bail-out. An involvement of the German carrier could circumvent EC rules.

Failing either option above (or any combination), the situation is likely headed towards a dual process in Latvia and Ch11 (aircraft leases). Bonds have security worth approx. 15c/€ and arguably, a recovery based on that alternative scenario is the outcome investors need to be prepared for.

-

Altice Intl.: It is impossible to separate Altice International from its more troubled sibling, Altice SFR, which results in depressed prices for the Altice International structure. The level of fear is highlighted by the fact the 4-month, fully cash-collateralised, near-term bonds still trade at 7%. Everything else is priced back of this.

Upside: The Company are seeking to differentiate between both silos and any meaningful (legal) efforts should see both seniors and subs trade up, to those seen before the call. However, with leverage likely to remain in the 4.0-4.5x range, the seniors' upside is c. 5-8pts, which would bring yields back to c. 8% from the current 10-11%. Sub bonds, due to their size will be more volatile, but a 15% YTM is easily attainable, implying 10pts plus upside.

The downside is centred on adverse shareholder actions, but from current levels, we see limited downside for seniors and subs. The risk of Drahi plundering the business is small, given he already relies on the dividend stream he achieves from the company.

-

SFR Altice France: Bluntly, we view it as un-investible at the moment. The cat can be made for the seniors, at c. 70%, on the back of sum-of-the-part estimations and the fact that they are trading at “recovery” values. However, we are taking a more cautious view, especially given the poor performance, and although recovery may be in the 70’s, this is very much an upside scenario. The downside has increased, possibly even 20pts, as maturity extensions and partial debt forgiveness appear to be already seen as the base case scenario.

The subs remain a binary trade. The downside is zero, with sub-bond holders having limited control in any proceedings. Upside could be 10-20pts, but very much at the discretion of the Company via a generous tender offer or a pact between Senior and Subordinated bondholders.

-

Amara: The bonds earn a running yield of 20%, which should prevent them from falling much further for the time being, as Amara has enough liquidity to avoid having to approach its creditors for the foreseeable future.

- On the upside, the business has merely had to re-settle into a normal energy price background. The down-cycle of solar on the back of postponed climate goals is so far more a spectre than reality and Amara generally operates in a growth sector.

- On the downside, this company will probably have to restructure in two year's time. So we would not expect bonds to return to a yield-driven price-range unless the macro environment turns out much better than we fear.

-

Antolin: Both bonds have been trading on top of one another, despite the long-dated bond sporting the far higher coupon. The company needs to address its balance sheet. Having received incurrance covenant waivers for all of 2026, it faces a springing maturity form banks in October ’27, one year ahead of the ‘28s. Antolin has amassed a small cash warchest from asset sales, and management are considering all options - except fresh cash from the family, a well that should have run dry long ago.

So it is likely that the forthcoming proposal will seek to apply one sweeping fix to the balance sheet, addressing the bank debt and the bonds - possibly pushing maturities out, not much more. But if creditors block, the family will seek to retain control for as long as possible and that could mean it turns to addressing the front-end, the ‘28s.

Two scenarios: (1) A single proposal is approved, both bonds rise from the low 60s to the mid 70s (the company is still not making any money). (2) Antolin is forced to address the front end. The ‘28s rocket into the 80s and beyond, while the ‘30s are left holding the bag, falling into the 40s and below.

-

Atalian: We value Atalian bonds at 50c/€ on a DCF basis. Whilst this is a significant premium to the current price of 25c/€, we do not see a deal to sell the business or an A&E giving bondholder equity as likely in the near term. We see 5 points of downside as the bonds will continue to drift lower until the company approaches bondholders. We do not expect any positive moves by management until after the FY results in late March, and we will revisit after that.

-

Branicks: We see a fair value of the bonds at 80c/€, whilst they currently trade at 73c/€. We see 7 points of upside in the bonds and 15 points of downside in the short term as Branicks seeks to move forward with an A&E operation for the SUNs. Our core thesis is that creditors will agree to a consensual rescheduling of debt, but there are questions about the availability of the StaRug process, which will cause volatility for the SUNs in the near term. We cannot rule out a non-consensual German liquidity, but we think it is unlikely, given the damage to the interests of all creditors. We expect the A&E will offer bondholders and promissory note holders a partial redemption in return for a four-year extension, with the package valued at 90c/€ to avoid being classified as being viewed as coercive.

-

Cerba: In the near term, tightly held debt limits immediate downside to 5–10 points, though adverse French regulatory shifts remain a risk. Conversely, the necessity of a comprehensive balance-sheet overhaul caps upside at roughly 80 (c. 5 points). Longer-term, achieving a sustainable capital structure would require equitising 50% of the senior debt, creating up to 20 points of downside. Our recapitalisation scenario envisages a €300m super-senior cash injection, further reducing the sustainable residual debt load.

Ultimately, this process requires fresh capital; creditors participating in a new-money solution will likely see superior recoveries.

-

Emeria: From what we gather, there must already be a deal in place, and we expect it to keep all creditors in one class. Most of this class should be made up of the term loans and the now fully drawn RCF, so the SSNs may have a weak standing where they may be looking to protect their SUN x-holdings.

The SSNs are value covered, and we see downside in the 70s, allowing for a 25% equity cushion and just about covered FCCR at what could be the trough earnings. On the upside, we expect the SSNs to remain unimpaired through the process and pari passu (real pari passu) with the rest of their class.

-

Graanul: Upside: Only from a successful refinancing in the next couple of weeks. Par is the upside, but the probability of execution remains low.

Downside: In the absence of a refinancing, we expect bonds to trade in the low-90s. Overcapacity in the wood pellet market is likely to pressure FY27 volumes and pricing, although secured 2026 volumes provide some downside protection.

-

Ineos Group: In the short term, we see limited idysiocratic risk, resulting in Ineos bonds likely to trade in a narrow range. Medium-term upside on the back of a more positive outlook will result in the bonds trading inside 10%, implying 5- 7 pts across the structure.

Until we come closer to the front-end of its maturity stack in 2029, the downside is likely to be limited to a 15% yield, especially given its adequate liquidity profile. This would result in 5 pts of downside.

-

Ineos Quattro: Ineos Quattro is expected to generate EBITDA above historic highs, supporting current bond prices. However, upside is limited to c. 7 to 8% yield, or 5 to 8 points, as Ineos Quattro remains highly GDP sensitive. While near-term dislocations are supportive today, the business does not deleverage sufficiently to offset the negative impact of the conflict on longer-term economic growth.

Downside: Absent a resolution to the conflict, we see limited downside from current levels. However, if the conflict were to end and trade flows normalise before the end of 2026, EBITDA would likely return to recent lows. In this scenario, we would expect a price decline of 10 to 15 points, returning to the trading levels experienced in January and February.

-

Isabel Marant: The Company has positive momentum, and under optimistic assumptions, the enterprise value exceeds total debt. However, we see limited upside above 80 given weaknesses in the debt documentation. With no near term triggers, the bonds may trade in the 70s for the coming months.

Downside could ultimately be 30pt to 40pt, but in the short term, with no imminent maturities, the risk before FY25 results in April is limited. The larger downside risk is tied to an eventual restructuring, as EBITDA growth is unlikely to reach a level that would allow for a refinancing.

-

Kem One: From current levels (c.30c/€), it is difficult to project any upside from the bonds specifically. There will be a further restructuring, and bondholders may be in a position to provide fresh cash and obtain the majority of the equity via for debt-for-equity swap. However, with a significant super senior facility ahead of the bonds, the doomsday scenario of a zero recovery is possible. With the requirement of fresh cash, the downside is realistically another 20pts.

The PVC market can rebound quickly, but from current levels, there is limited upside in the short term.

-

Klockner Pentaplast: The process risk embedded in the current CH11 Prepack is probably contained. On the upside, 1L creditors should recover 36c/€ in new Exit Financing, priced at 8% coupon for 1.5x projected FCCR from 2027. 1Ls also receive 100% of the equity, but at a price of 42c/€, holders of this tranche (class 3) already pay for 20% of that equity.

The fresh cash, which is reserved for participants in the Bridge facility (check your upstream) receives a mere 5% PIK over the future interest it will earn in common with the pari passu reinstated 1L above. So it is unlikely to trade up following the conclusion of the Texas process.

On the downside, we have not had fundamental business data in a year. We have theories for what the structural headwinds could be, but no confirmation. Should they materialise, the company may yet again prove overleveraged.

-

Lowell: The New Money Notes will recover par under all circumstances..

On the upside, the SSNs may hope for a sale of the business, in which case they might be treated pari passu to one another and therefore recover potentially as much as 45p/£.

On the downside, in a multi-staged restructuring process, non-participating SSNs face full wipe-out and must accept nuisance value in an ultimate UK RP.

-

Matalan: Matalan needs to extend its maturities, and the previous SSN holders remain in control across the capital structure. Even though there is room under the covenants, the need for an incremental £35m short-term facility to help fund its ambitious growth plan and associated WC outlay could well be the trigger to effect the wider transaction.

The SSNs will likely remain unaltered, safe for the longer maturity. Danger could come from any uneven distribution between shareholders and SSN holders now, whereby the former could benefit in their left pocket from reducing the value in their right pocket, respectively. However, we think this is unlikely.

For now, we value the SSNs (EV covered) on their running yield of nearly 15%. This could rise going into the transaction, but should recover thereafter.

Matalan have an overall good chance to refinance this bond in 2-3 years’ time.

-

Maxeda: At 91, the bonds have up to nine points of upside if private creditors refinance the company. That being (despite the boom) somewhat unlikely, a more reasonable upside would be in the mid-90s, since a HY transaction would probably have to be an A&E with a sub-par outcome.

On the downside, a Debt/Equity swap is becoming more likely, which should result in reinstated debt worth no more than 75-80c/€. The company has had time to broker a deal all 2025, while LfLs were positive and the market was open. Now the market has swung against marginal refi bets, and a deal would have to be reached by March 2026.

-

Mobico: Perps are just about EV covered, containing an element of equity, which is reflected in their price. The high coupon on the perps following the call date is about adequate for the leverage. If the company can contain the Spanish deregulation and execute on the German settlement, the UK asset sale/financing and the US WMATA litigation, then the perps could trade at par next year. These milestones are not far-fetched, and once realised, we see the business in a better position to address its balance sheet, for which it is already hoarding ample liquidity. We draw confidence from the decisive stabilisation management has brought about in the last six months.

On the downside, the Perps have no protection other than their sheer size and inconvenience to the shareholders.

-

Pfleiderer : These bonds are unlikely to be refinanced in an orderly way at maturity. The drop-down of Silekol has provided the company with enough cash to last for another two years, by which time there should have been sufficient turnaround in its downstream market to allow a valuation on some positive cash flow generation. The documentation allows for another LME, but that may yet be a moot point if shortly afterwards maturities loom. In that context, it’s important to bear in mind that two bondholders are said to hold some 55% of the notes and could find a loophole through the anti-non-pro rata provisions that were agreed in the first A&E.

Bonds should continue to trade on a break-up valuation without factoring in the cash balance that will likely be spent over the next two years. The current price of 43c/€ approx. represents that, but on the bullish side. Upside comes from fundamental recovery and any bondholder’s ability to either defend themselves (through size) from other bondholders, or to trade out before the start of the next round. In the interim, bond interest is effectively cash funded.CC+, No Book, Blue, Event Driven

These bonds are unlikely to be refinanced in an orderly way at maturity. The drop-down of Silekol has provided the company with enough cash to last for another two years, by which time there should have been sufficient turnaround in its downstream market to allow a valuation on some positive cash flow generation. The documentation allows for another LME, but that may yet be a moot point if shortly afterwards maturities loom. In that context, it’s important to bear in mind that two bondholders are said to hold some 55% of the notes and could find a loophole through the anti-non-pro rata provisions that were agreed in the first A&E.

Bonds should continue to trade on a break-up valuation without factoring in the cash balance that will likely be spent over the next two years. The current price of 43c/€ approx. represents that, but on the bullish side. Upside comes from fundamental recovery and any bondholder’s ability to either defend themselves (through size) from other bondholders, or to trade out before the start of the next round. In the interim, bond interest is effectively cash funded.

-

SBB: The Community Assets deal has provided an additional SEK11bn in liquidity to meet maturities through the EUR 2.25 Jul 27 bonds (SEK7.5bn outstanding). The 2027 bonds are trading inside 6.5% so they offer little value. The SEK7.3bn €0.75% bonds due in November 2028 are trading at a YTW of 7.5% (82.7c/€). The SEK7.3bn €0.75% bonds due in November 2028 are trading at a YTW of 7.5% (82.7c/€). We see a potential for 10 points of upside and 6 points of downside if they trade out to >10%. We expect that SBB will need to deal with this maturity by selling parts of its stakes in Community/Residential (or Education to Brookfield), as the alternative is hoping a rising Real Estate market bails them out. SBB doesn’t need to rush this fence, so the upside will take time to come

-

Selecta: Following an exceptionally disappointing quarter and news that the company has hired advisors, we conclude that the A&E we were previously envisioning will likely give way to a full-blown restructuring.

We see the SSNs as unimpaired - possibly receiving 5% in cash to extend 95% of their exposure. The 2LNs should receive some 60c/€ in new bonds, a good 10% in cash and some 30c/€ worth of new equity. There should further be an opportunity across classes to participate in the fresh cash that is funding the above pay-downs and is receiving primarily equity and, together with any other equity, receiving control in return.

Upside comes from a renewed injection by shareholders KKR, whereas downside should be mostly driven by inter-creditor negotiations and any fundamental weakening of a credit that is set to suffer from low and falling consumer confidence on the continent.

-

Upside: Our DCF results in an EV of €300-350m, which theoretically results in a par recovery. However, with fresh capital required, the majority of value could leak to new money providers. The realistic upside is 30-40 points, based on the debt capacity of Standard Profil based on FY25 figures, which is predicated on new money injection. The timeframe for any positive recovery will be long, as the value will only accrue once the OEM orders are converted into cash, which is late FY25/FY26.

Downside: Given the lack of senior debt, and the strength of the order book, we see limited downside at the current prices. Bondholders are in a strong position to provide the additional liquidity and we see 10pts max of downside from current levels.

-

Stonegate: Priced apparently as an 11% yield name, Stonegate is not that. The company is losing too much cash too fast to hold together through maturities setting in at company level by 2029. The company will have to sell assets to raise liquidity - we don’t believe the shareholders will inject more funds. The shape of the deal will determine what Stonegate do with any cash and what a future company and balance sheet might look like. The strong asset coverage from the pub estate limits downside in the name.

-

Synthomer: At 76c/€, the Synthomer bonds are no longer a short, with ample liquidity and loosened bank covenants, the company has time to await the strengthening of margins and some volume growth into H2. The uncertainties around the Gulf conflict mean we do not expect progress towards a Fair Value over 80c/€. The SUNs have been layered as the banks have been given security, but we still see significant FV upside in the next 18 months.

-

Tele Columbus: Fair value of the bonds around the current price of 65c/€. We see 10 points of upside if TC raises fresh cash and customer additions improve in line with our model; this would be a return to where the bonds traded before the disappointing Q1 results. In contrast, there are 3 points of downside if the bonds trade to their fair value. We forecast that €100m of fresh cash will be needed by Q3 2026 (€50m in Fresh cash and €50m in proceeds from the sale of the Magdeburg asset). Tele Columbus has options, but they are difficult and will be expensive. The current bond pricing points to market scepticism that the build-out will be funded. The debt load is unsupportable, so a debt equity swap will be needed.

-

Thames Water: The Class A debt should be reinstated with a stub worth approx. 70cp/£. We see a downside around 60p/£ and an upside of approx. 78p/£ if creditors receive a bigger sliver of equity. For an unlikely, but still possible Special Administration followed by Nationalisation, the downside for creditors is be hard to measure. We see the reinstated stub paying approx. 5.75% coupon and the equity yielding just over 10%.

-

Transcom: The bonds have risen to 85%, potentially due to short covering. A realistic upside is 5pts under our base case scenario, where the bonds are extended c.3yrs with a similar coupon. The bonds should trade at 10-12% yield to the new maturity, implying a c. 90% bond price. There is the theoretical upside of 15 points in the event of a par refinancing, especially if Altor provide additional equity. But we see this as unlikely.

The downside risk has lessened somewhat due to the recent operational rebound, although an assertive stance from the sponsor could still lead to bond prices declining by 10 to 15 points.

-

Tullow: Theoretical upside remains par, based on asset net present value, but in practice, we expect the bonds to remain anchored in the low-80s until the company delivers concrete progress on asset disposals. Even if a transaction materialises, unresolved tax disputes and significant decommissioning liabilities could materially erode recoveries.

Downside risk remains substantial and could exceed 20 points. An adverse outcome in the tax arbitration would raise serious questions around directors’ duties and the risk of trading while insolvent. Given the fragility of the capital structure and ongoing solvency concerns, we find it surprising that the company has not pursued a delisting.

-

Ubisoft: On the upside, we are seeing the company raise financing at a MidCo with a share pledge on the Vantage Studio assets to pay down the bonds at par and at maturity. the ‘27s should trade up ahead of that on news of that liquidity arriving.

On the downside, we see these bonds asset covered, since an insolvency threat to the bonds remains blunt and therefore an LME could not leverage it to force a large discount. At most, a simultaneous voluntary offer in the 70s to both bonds could put pressure on the '27s to follow the '31s. The '31s are a more fundamental bet on the ambitious turnaround.

-

Victoria Plc :Victoria requires significant uptick in volumes to even come close to growing into its capital structure. We envisage the 1PN Notes to be partially equitised ahead of maturities in 2028, as per our projections, leaving the bonds with further downside. This could be 10-15pts, especially if fresh cash is provided on terms that are to the detriment of 1PN holders.

The Original Notes (2028 Notes), trade at 17c, and have limited upside unless they can successfully challenge the prior uptiering, especially if cash runs out within the look-back period. . The downside for the Original 2028 Notes is zero, as a full equitisation is the most likely outcome.

LEGEND

📕 icon indicates credits currently on our book, please see Track Record.

Likelihood of restructuring/LME process within 18 months: 🟦 Current 🟩 Unlikely 🟧 Potential 🟥 Certain

NAMES UNDER CONSIDERATION

Tereos

SARRIA News Flow